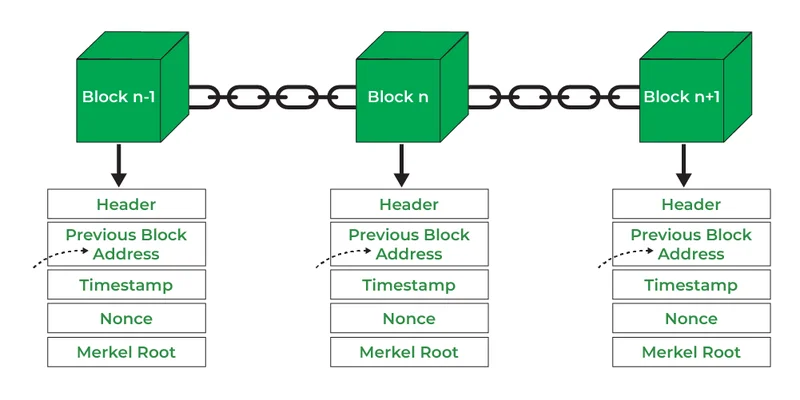

Blockchain: The Next Step in Growth Story?

Alright, let's talk about HIVE Digital Technologies. The narrative floating around is that they're brilliantly positioning themselves at the intersection of Bitcoin mining and AI, fueled by renewable energy. A compelling story, no doubt. But let's dig into the numbers and see if the reality matches the hype.

Mining and AI: A Question of Synergy

HIVE is touting its expansion into AI-ready data centers alongside its Bitcoin mining operations. They've reached 23 Exahash per second in mining capacity, a respectable figure. And the purchase of 32.5 acres in Grand Falls for Tier III+ AI data centers is certainly a tangible investment. The question is, does this dual approach make strategic sense, or is it simply a case of trying to ride the AI wave?

The company claims this expansion could be a "significant short-term catalyst." Maybe. But catalysts need fuel, and in this case, that fuel is capital.

The Dilution Dilemma

This is where my eyebrows start to raise. The Simply Wall St analysis points to a potential "deflated share price" compared to its estimated value. Okay, fair enough, valuations are always subjective. But the mention of "dilution risk" is hard to ignore.

The analysis explicitly states that a shelf registration filing signals potential future equity or debt issuance, which may lead to more shareholder dilution. And let's be frank, the insider selling and dilution over the past year are already "key worries."

Now, companies often need to raise capital for expansion. That's not inherently a bad thing. But when you're chasing two very capital-intensive sectors simultaneously—Bitcoin mining and AI infrastructure—the need for cash becomes even more pressing. The question becomes: At what cost?

The Terbium Twist

There's also this interesting tidbit about GPUs needing Terbium, a rare earth metal. The article mentions only 37 companies in the world are exploring or producing it. I'm not saying HIVE is directly involved in Terbium mining, but it highlights the complex supply chain dependencies involved in the AI hardware space. If access to this rare earth metal becomes a bottleneck, it could impact HIVE's ability to scale its AI operations.

And this is the part of the report that I find genuinely puzzling. If HIVE is aiming for high-performance, clean computing, what is the plan to ensure they have access to the resources required to make that happen?

Community Sentiment: A Grain of Salt

The article mentions "extremely wide ground" among fair value opinions, ranging from US$3.46 to US$34.63. That's a tenfold difference! Such a massive discrepancy suggests a high degree of uncertainty and speculation surrounding HIVE's future prospects. It's also worth noting that "recent news and potential dilution risk could heavily influence sentiment and future value debates." Translation: People are nervous.

A Calculated Gamble or a Desperate Throw?

HIVE's move into AI could be a strategic masterstroke, positioning them for long-term growth in a rapidly evolving landscape. Or, it could be a case of spreading themselves too thin, diluting shareholder value, and struggling to compete in two highly competitive industries. The numbers, as always, tell a more nuanced story than the headlines.

My analysis suggests that while the vision is compelling, the execution hinges on their ability to manage capital effectively and navigate the complex supply chains of the AI hardware market. And, if they aren't able to do either of those things, the company may have just made a desperate throw.

Is It Really a Bargain?

According to Is HIVE Digital Technologies (TSXV:HIVE) Blending Blockchain and AI the Next Step in Its Growth Story?, HIVE is attempting to blend blockchain and AI as the next step in its growth story.

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

The Manyu Phenomenon: What Connects the Viral Crypto, the Tennis Star, and the Anime Legend

It’seasytodismisssportsasmer...

-

The Nebius AI Breakthrough: Why This Changes Everything

It’snotoftenthatatypo—oratl...

-

ASML's Future: The 2026 Vision and Why Its Next Breakthrough Changes Everything

ASMLIsn'tJustaStock,It'sthe...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

- Search

- Recently Published

-

- Misleading Billions: The Truth About DeFi TVL - DeFi Reacts

- Secure Crypto: Unlock True Ownership - Reddit's HODL Guide

- Altcoin Season is "here.": What's *really* fueling the latest altcoin hype (and who benefits)?

- The Week's Pivotal Blockchain Moments: Unpacking the breakthroughs and their visionary future

- DeFi Token Performance Post-October Crash: What *actual* investors are doing and the brutal 2025 forecast

- Monad: A Deep Dive into its Potential and Price Trajectory – What Reddit is Saying

- MSTR Stock: Is This Bitcoin's Future on the Public Market?

- OpenAI News Today: Their 'Breakthroughs' vs. The Broken Reality

- Medicare 2026 Premium Surge: What We Know and Why It Matters

- Accenture: What it *really* is, its stock, and the AI game – What Reddit is Saying

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Plasma (4)

- Zcash (7)

- Aster (10)

- qs stock (3)

- mstr stock (3)

- asts stock (3)

- investment advisor (4)

- morgan stanley (3)

- ChainOpera AI (4)

- federal reserve news today (4)