Broadcom's OpenAI AI Chip Deal: Analyzing the Stock's New Valuation and Future Forecast

Broadcom’s OpenAI Deal Is More Than a Win—It’s a Declaration of War

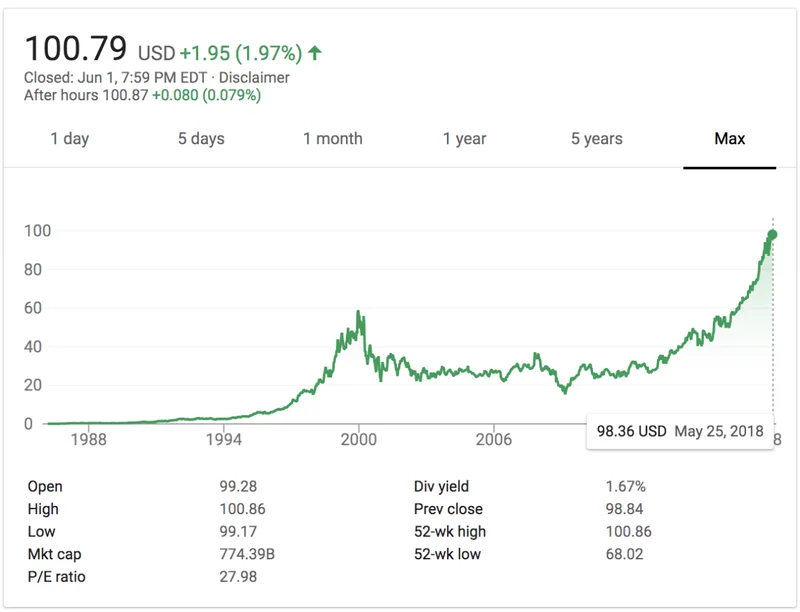

The market’s reaction on October 13th was predictable. A confirmed partnership with OpenAI sent Broadcom’s stock (AVGO) surging nearly 9%, capping a year where its valuation has already swelled to a staggering $1.6 trillion. On the surface, this is just another chapter in the great AI gold rush: a critical supplier lands the industry’s marquee customer. The financial filings support the euphoria, with record backlogs and AI-related sales surging 63% year-over-year.

But to view this event as merely a blockbuster purchase order is to miss the plot entirely. The press release and subsequent commentary weren’t about a simple transaction. They were a carefully worded manifesto. When OpenAI’s CEO says designing your own chips lets you "control your destiny," and Broadcom’s CEO speaks of co-developing the "future of AI," they are signaling a fundamental realignment in the hardware power structure. This isn't just a deal. It's a declaration of independence from the GPU monoculture, and Broadcom is supplying the armaments.

Deconstructing the 10 Gigawatt Handshake

Let’s be clear about what was announced. This is a multi-year, strategic collaboration to deploy 10 gigawatts of custom AI accelerators. That figure—10 gigawatts—is the most important number in the release, OpenAI, Broadcom Announce 10GW AI Accelerator Deployment. It isn't a dollar amount; it's a unit of power, a proxy for a truly colossal amount of computational capacity. For context, a large nuclear power plant produces about one gigawatt. OpenAI and Broadcom are planning to build and deploy an AI infrastructure with an energy appetite equivalent to a small nation, with deployments starting in late 2026.

This isn't about OpenAI simply buying Broadcom's off-the-shelf parts. OpenAI is designing the accelerator architecture itself, embedding its unique learnings from building frontier models directly into the silicon. Broadcom’s role is that of the world’s most sophisticated foundry and systems integrator, taking OpenAI’s blueprint and turning it into functional, scaled-out data center racks connected by its best-in-class Ethernet fabric.

This is the new paradigm. Think of it less like buying a car and more like a Formula 1 team co-designing a bespoke engine with a specialist manufacturer. While Nvidia sells a world-beating engine to any team that can afford it, Broadcom is the partner that helps you build your own unique engine, tailored to your specific racing strategy. This is precisely what it's already doing for Google's TPUs and Meta's custom silicon efforts. The OpenAI partnership solidifies Broadcom's position as the premier enabler of "sovereign compute" for the hyperscalers. They are no longer just component suppliers; they are kingmakers.

The financial data reflects this strategic capture. Wall Street analysts, caught up in the announcement, are now scrambling to revise their models, with firms like Bernstein projecting Broadcom’s AI-related revenue could exceed $40 billion in fiscal 2026, up from a $30 billion forecast just weeks ago. The company’s record $110 billion backlog provides the visibility to support these claims. The question is, what is the market paying for this dominant position?

The Price of Flawless Execution

This is the part of the analysis that gives me pause. Broadcom's operational performance is, without question, exceptional. But its current valuation has extrapolated that performance into perpetuity, leaving absolutely no margin for error. The stock’s run-up in 2025 was roughly 90%—to be more precise, it nearly doubled from its April lows to its October peak. This has pushed its valuation metrics into territory that demands nothing short of perfection.

Its price-to-sales ratio now sits at approximately 25x, a stark deviation from its historical average of under 10x. On a forward-looking basis, its non-GAAP P/E ratio is in the mid-30s, right in line with Nvidia. (The trailing GAAP P/E of ~85x is largely distorted by non-cash amortization charges from the massive VMware acquisition, a deal that now supplies nearly half its revenue from high-margin software). While the software business provides a stable foundation, the market is clearly pricing the stock based on its AI chip growth story.

I've looked at hundreds of these semiconductor filings, and the speed at which forward estimates for Broadcom have been revised upwards is something I've rarely seen. Yet the stock price has moved even faster, effectively pricing in not just 2026's success, but likely 2027's as well. This creates a precarious situation.

The market is betting on flawless execution of a multi-year, incredibly complex engineering project that won’t even begin deployment for another two years. What happens if there are integration challenges with OpenAI’s design? What if the broader macroeconomic environment, already showing signs of strain from U.S.-China trade tensions, deteriorates further? We saw a preview of this fragility on October 10th, when renewed trade fears sent the Nasdaq down 3.6% and briefly knocked AVGO below its 50-day moving average. In a market priced for perfection, any small disappointment can trigger a disproportionately severe correction.

A Bet on Balkanization

Ultimately, buying Broadcom at these levels is not a bet on its next earnings report. It’s a structural bet on the balkanization of the AI hardware market. It’s a wager that the future of AI compute won’t be a monopoly controlled by one GPU provider, but a multi-polar world where every major player—Google, Meta, Amazon, and now OpenAI—demands its own custom-built silicon to gain a competitive edge.

In that world, Broadcom is the indispensable partner, the quiet enabler behind every throne. The market has correctly identified this role and has awarded the company a kingmaker's premium. My analysis suggests, however, that this premium has now fully priced in the coronation, the reign, and the succession plan. The narrative is compelling, but the numbers demand a level of execution that even the most dominant companies find difficult to sustain. The war for AI supremacy is just beginning, and this valuation already assumes the victor has been decided.

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

ASML's Future: The 2026 Vision and Why Its Next Breakthrough Changes Everything

ASMLIsn'tJustaStock,It'sthe...

-

Morgan Stanley's Q3 Earnings Beat: What This Signals for Tech & the Future of Investing

It’seasytoglanceataheadline...

-

The Manyu Phenomenon: What Connects the Viral Crypto, the Tennis Star, and the Anime Legend

It’seasytodismisssportsasmer...

-

The Nebius AI Breakthrough: Why This Changes Everything

It’snotoftenthatatypo—oratl...

- Search

- Recently Published

-

- Misleading Billions: The Truth About DeFi TVL - DeFi Reacts

- Secure Crypto: Unlock True Ownership - Reddit's HODL Guide

- Altcoin Season is "here.": What's *really* fueling the latest altcoin hype (and who benefits)?

- The Week's Pivotal Blockchain Moments: Unpacking the breakthroughs and their visionary future

- DeFi Token Performance Post-October Crash: What *actual* investors are doing and the brutal 2025 forecast

- Monad: A Deep Dive into its Potential and Price Trajectory – What Reddit is Saying

- MSTR Stock: Is This Bitcoin's Future on the Public Market?

- OpenAI News Today: Their 'Breakthroughs' vs. The Broken Reality

- Medicare 2026 Premium Surge: What We Know and Why It Matters

- Accenture: What it *really* is, its stock, and the AI game – What Reddit is Saying

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Plasma (4)

- Zcash (7)

- Aster (10)

- qs stock (3)

- mstr stock (3)

- asts stock (3)

- investment advisor (4)

- morgan stanley (3)

- ChainOpera AI (4)

- federal reserve news today (4)