The ARM Stock Hype Train: Is This an AI Revolution or Just Another Bubble?

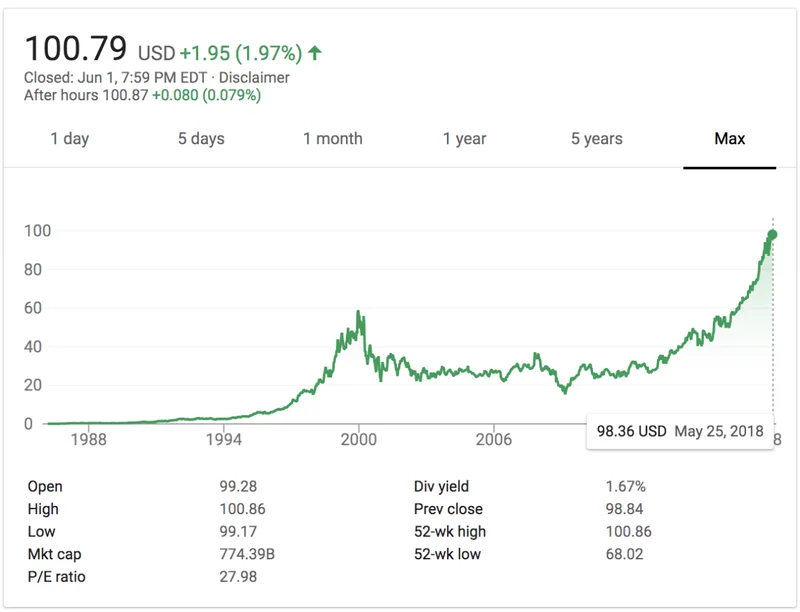

So, let's talk about ARM. Looking at its stock chart is like watching a cardiogram during a panic attack. One day it’s up 11% (ARM (NASDAQ:ARM) Shares Up 11.1% - Here's What Happened), the next it’s taking a nosedive. The talking heads on financial TV are screaming "AI revolution!" while the numbers guys are quietly pointing at a price-to-earnings ratio that looks more like a zip code.

The big question everyone's whispering is the one right in the title: Is this whole thing a genius-level play unfolding before our eyes, or are we all just watching a beautifully engineered bomb count down to zero?

I’ve been staring at the data, the press releases, the analyst reports filled with their safe "Moderate Buy" ratings, and I gotta be honest—it smells funny. It smells like a whole lot of hype being pumped into a very small balloon, and we all know what happens to those.

The 'Switzerland of Semiconductors' Narrative

Okay, let's give the bulls their moment. The argument for ARM being a genius play is, on the surface, pretty damn compelling. This company is basically the ghost in the machine. They don't make the chips; they design the fundamental architecture that goes into practically every smartphone on the planet. A 99% market share? That's not a business, that's a global standard. It's like owning the patent on the concept of a wheel.

Their business model is the envy of the tech world. They just sit back, design brilliant, power-efficient blueprints, and collect royalties from giants like Apple, Qualcomm, and Samsung. With gross margins floating around 97%, they're essentially printing money. No messy factories, no supply chain nightmares. It's beautiful.

And now, they're pivoting hard into the AI gold rush (Arm Holdings’ AI-Powered Rally: Stock Surges Amid SoftBank’s Big Bet and Tech Partnerships). They're pushing their Neoverse chips for data centers and launching new platforms like "Lumex" for on-device AI. The story they’re selling is that every single AI-powered gadget, from your phone to your car, will have to pay the ARM toll. It’s a powerful narrative, and it’s what’s fueling this insane rally. You can almost see the PowerPoint slide in the boardroom: "We are the picks and shovels of the AI revolution."

But does being the "Switzerland of semiconductors" justify a valuation that makes Nvidia look like a value stock? Are we really supposed to believe that a company chained to the slow-growth smartphone market can suddenly grow into a valuation north of $180 billion without a hitch? I mean, come on.

This is where the story starts to fray at the edges for me. It’s a little too perfect, a little too clean. It feels like I'm being sold something, and I've learned that when a story is this good, you better start looking for the catch.

SoftBank's Private Piggy Bank

Here’s the catch. His name is Masayoshi Son, and his company, SoftBank, owns 90% of ARM.

This isn't a normal public company. It's a company with a tiny, 10% free float, which means the stock price is a complete fiction. It’s like judging the value of a Picasso by the price someone paid for a single brushstroke. The slightest bit of news—a new deal with Qualcomm, a rumor about a server chip—sends the stock flying because there are so few shares to trade. The volatility isn't a bug; it's a feature.

And SoftBank is using this feature to its full advantage. They just arranged another $5 billion margin loan, using their ARM stock as collateral. Add that to previous deals, and they're looking at nearly $18.5 billion borrowed against a stock whose price is based on a sliver of available shares. This is not a healthy sign. This is a sign that ARM is being used as SoftBank's personal ATM to fund its other wild AI bets.

What happens if one of those bets goes south? What happens if SoftBank needs cash and starts to unload shares, or if a margin call comes knocking? The 10% of investors who think they own a piece of a stable tech giant will find out they were just along for the ride in someone else's souped-up, highly leveraged sports car.

This is a bad setup. No, "bad" doesn't cover it—this is a five-alarm dumpster fire of corporate governance. You have a parent company with a history of spectacular flameouts using its prize asset as collateral for a high-stakes poker game. Meanwhile, ARM is picking fights with its biggest customers, like the ongoing legal mess with Qualcomm. You’re suing the people who pay your bills while your majority owner is using you as a credit card. How does that end well? This whole thing ain't sustainable.

And don't get me started on the valuation. A P/E ratio over 200. Let me repeat that: two hundred. For a company with projected revenue growth around 20%. The math just doesn't work unless you believe in miracles, and I stopped believing in those around the same time I stopped believing in the dot-com bubble. Maybe I'm just too cynical, but this looks less like a genius investment and more like a cult. A very, very expensive cult. The whole thing seems offcourse.

They expect us to just ignore the fundamentals because of the magic word: "AI." And honestly...

It's a Shell Game, Not a Stock

Let's be real. ARM, the company, is a fantastic piece of engineering. They built an empire on efficiency and smart licensing. But ARM, the stock, is something else entirely. It’s a financial instrument being manipulated by a majority owner to fund a speculative venture capital crusade. The price you see on your screen has almost no connection to the company's actual performance or realistic future prospects. It’s a reflection of scarcity, hype, and the borrowing needs of Masayoshi Son. The ticking you hear isn't the sound of innovation; it's the sound of a margin call getting closer.

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

ASML's Future: The 2026 Vision and Why Its Next Breakthrough Changes Everything

ASMLIsn'tJustaStock,It'sthe...

-

Morgan Stanley's Q3 Earnings Beat: What This Signals for Tech & the Future of Investing

It’seasytoglanceataheadline...

-

The Manyu Phenomenon: What Connects the Viral Crypto, the Tennis Star, and the Anime Legend

It’seasytodismisssportsasmer...

-

The Nebius AI Breakthrough: Why This Changes Everything

It’snotoftenthatatypo—oratl...

- Search

- Recently Published

-

- Misleading Billions: The Truth About DeFi TVL - DeFi Reacts

- Secure Crypto: Unlock True Ownership - Reddit's HODL Guide

- Altcoin Season is "here.": What's *really* fueling the latest altcoin hype (and who benefits)?

- The Week's Pivotal Blockchain Moments: Unpacking the breakthroughs and their visionary future

- DeFi Token Performance Post-October Crash: What *actual* investors are doing and the brutal 2025 forecast

- Monad: A Deep Dive into its Potential and Price Trajectory – What Reddit is Saying

- MSTR Stock: Is This Bitcoin's Future on the Public Market?

- OpenAI News Today: Their 'Breakthroughs' vs. The Broken Reality

- Medicare 2026 Premium Surge: What We Know and Why It Matters

- Accenture: What it *really* is, its stock, and the AI game – What Reddit is Saying

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Plasma (4)

- Zcash (7)

- Aster (10)

- qs stock (3)

- mstr stock (3)

- asts stock (3)

- investment advisor (4)

- morgan stanley (3)

- ChainOpera AI (4)

- federal reserve news today (4)