Bloom Energy's Sudden AI Play: The Insane Stock Surge and Why I'm Not Buying It

So, Bloom Energy’s stock popped more than 25% on Monday. A cool quarter of its value, conjured out of thin air in a few hours. Why? Because they shook hands with a company called Brookfield and signed a piece of paper promising to spend $5 billion on "AI infrastructure."

Five. Billion. Dollars.

Let that sink in. This isn't a company that just cured cancer or invented teleportation. This is a fuel cell company. A very important, very complex fuel cell company, sure, but we're not talking about a fundamental shift in the laws of physics here. We're talking about a deal. A press release. And for that, the market decided Bloom was suddenly worth billions more than it was on Friday.

This is the world we live in now. The AI hype train has left the station, and it’s dragging every car it can find along with it, whether the wheels are bolted on or not. You sell power? Great. Just say it’s for AI. You make microchips? Fantastic, they’re AI microchips now. You sell artisanal pickles? You better believe they’re optimized by a proprietary algorithm to enhance neural-network-driven flavor profiles. The market eats it up every single time. And I’m just sitting here watching the madness, wondering when everyone else is going to wake up.

The Five Billion Dollar Napkin

Let's be clear about what this deal is. Brookfield, an asset management behemoth, is going to "invest" $5 billion to deploy Bloom's fuel cells for AI data centers. It sounds incredible. It’s a visionary partnership to power the future of intelligence itself! At least, that's what the PR team wants you to think while you’re hitting the ‘buy’ button on your trading app.

But what does it actually mean? Is this $5 billion in cash hitting Bloom’s bank account tomorrow? Or is it a long-term, milestone-based framework that might, if everything goes perfectly over many years, eventually add up to that headline number? The details, as always, are conveniently fuzzy. We know a European site is coming by "year-end," but beyond that, it’s all grand pronouncements and forward-looking statements.

This is like announcing you’re going to build the world’s tallest skyscraper without showing anyone the blueprints or the soil analysis. It’s pure narrative. And the narrative is intoxicating: AI is growing at an explosive rate, and these massive "AI factories" need a truly biblical amount of power. They need it clean, and they need it reliable. Bloom Energy steps in, a knight in shining, eco-friendly armor, ready to solve the problem. It’s a perfect story. Almost too perfect.

And Wall Street? They’re not just drinking the Kool-Aid; they’re hooking it up to an IV. Morgan Stanley jacks their price target from $44 to $85. UBS sees $105. Evercore ISI, not to be outdone, slaps a cool $100 on it. These aren’t small adjustments. This is a complete re-evaluation based on a single announcement. Does this feel like sober financial analysis, or does it feel like a FOMO-fueled frenzy?

A Look Under the Hood Reveals... Rust

Okay, so the story is great. But I’ve learned the hard way that the story and the balance sheet are often two completely different books. So I did the unthinkable: I looked at Bloom Energy’s actual financials. And folks, it ain’t pretty.

The revenue growth is there, I’ll give them that. Up nearly 18% over the last three years. People are buying their stuff. But making money? That’s another question entirely. Their pre-tax profit margin is a disastrous -15.5%. They have a net income of negative $42 million. This isn't a company printing cash; it’s a company burning it to grow. Which is a fine strategy, I guess, if you’re a startup in a garage. But Bloom has been around for a while.

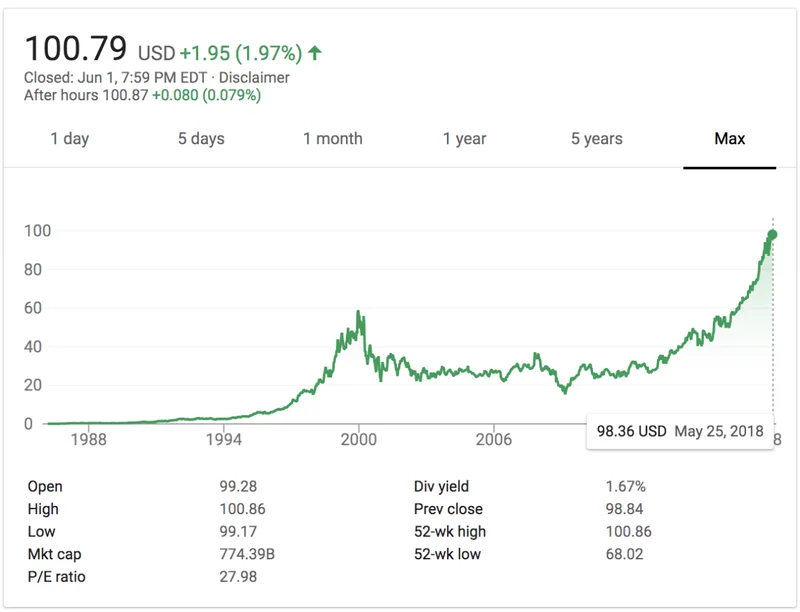

Then you get to the valuation. This is where it goes from questionable to outright comedy. A Price-to-Earnings (P/E) ratio of 789. That’s not a typo. 7-8-9. For context, a P/E of 20 is often considered reasonable. 789 suggests investors expect the company to grow at a rate that would make a god blush. It’s a valuation completely detached from current reality, floating in a sea of pure speculation.

This is a bad sign. No, "bad" doesn't cover it—this is a five-alarm dumpster fire of a metric. It’s a number that screams "bubble." It’s the kind of valuation that relies 100% on the story, because the numbers sure as hell don’t back it up. They’re selling a vision of 2028 where they've magically grown earnings by over $370 million, and everyone's buying it because the letters "A" and "I" are involved.

And what happens when the story hits a snag? What if the Brookfield deployment is slower than expected? What if a competitor comes along with a better, cheaper solution? The entire house of cards, built on a P/E of 789, could come crashing down. Then again, maybe I'm the crazy one for thinking a company should actually be profitable to be worth this much. Its a wild thought, I know.

So We're All Just Pretending This Makes Sense?

Let's cut the crap. Bloom Energy didn't become a fundamentally different company overnight. They signed a deal. A big, flashy, headline-grabbing deal that perfectly tapped into the market's insatiable, desperate hunger for anything related to AI. The stock isn't soaring because of proven profits or a technological breakthrough announced yesterday. It's soaring on pure, unadulterated hype.

This is a story stock, plain and simple. And right now, it’s telling the best story in town: Bloom Energy soars more than 20% on deal with Brookfield to put fuel cells in AI data centers. But stories end. Hype fades. And when the music stops, all you’re left with are the fundamentals. And Bloom's fundamentals are telling a very, very different story than its stock chart. Buyer beware.

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

ASML's Future: The 2026 Vision and Why Its Next Breakthrough Changes Everything

ASMLIsn'tJustaStock,It'sthe...

-

Morgan Stanley's Q3 Earnings Beat: What This Signals for Tech & the Future of Investing

It’seasytoglanceataheadline...

-

The Manyu Phenomenon: What Connects the Viral Crypto, the Tennis Star, and the Anime Legend

It’seasytodismisssportsasmer...

-

The Nebius AI Breakthrough: Why This Changes Everything

It’snotoftenthatatypo—oratl...

- Search

- Recently Published

-

- Misleading Billions: The Truth About DeFi TVL - DeFi Reacts

- Secure Crypto: Unlock True Ownership - Reddit's HODL Guide

- Altcoin Season is "here.": What's *really* fueling the latest altcoin hype (and who benefits)?

- The Week's Pivotal Blockchain Moments: Unpacking the breakthroughs and their visionary future

- DeFi Token Performance Post-October Crash: What *actual* investors are doing and the brutal 2025 forecast

- Monad: A Deep Dive into its Potential and Price Trajectory – What Reddit is Saying

- MSTR Stock: Is This Bitcoin's Future on the Public Market?

- OpenAI News Today: Their 'Breakthroughs' vs. The Broken Reality

- Medicare 2026 Premium Surge: What We Know and Why It Matters

- Accenture: What it *really* is, its stock, and the AI game – What Reddit is Saying

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Plasma (4)

- Zcash (7)

- Aster (10)

- qs stock (3)

- mstr stock (3)

- asts stock (3)

- investment advisor (4)

- morgan stanley (3)

- ChainOpera AI (4)

- federal reserve news today (4)